One of the biggest questions buyers are asking right now:

Should I go fixed or variable?

With mortgage rates stabilizing in 2026, the decision isn’t as obvious as it used to be.

Both options come with trade-offs — and the “right” choice depends on your situation.

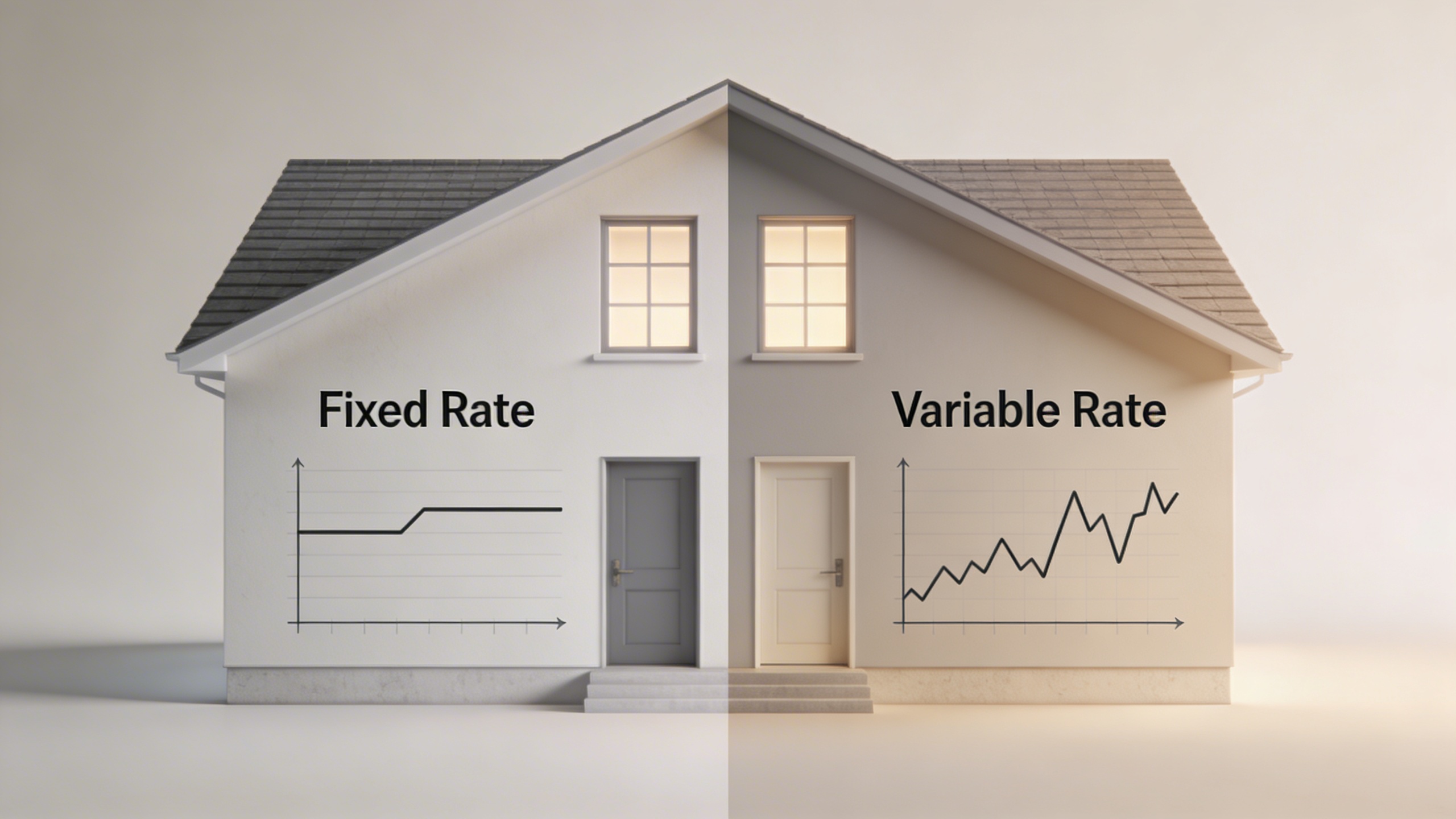

Fixed Rates: Stability and Predictability

Fixed-rate mortgages are popular for one reason:

👉 consistency

Your rate stays the same for your term, which means:

- predictable monthly payments

- protection if rates rise

- easier budgeting

This option works well if you value peace of mind and long-term stability.

Variable Rates: Flexibility and Opportunity

Variable rates can move with the market.

Right now, with rates expected to stay relatively stable or gradually decline, some borrowers are considering variable options again.

Benefits include:

- potential savings if rates drop

- more flexible penalties

- opportunity to adjust strategies

But the trade-off?

👉 uncertainty

What Borrowers Are Doing in 2026

Many buyers today are taking a more balanced approach:

- choosing shorter fixed terms

- considering variable with caution

- focusing on flexibility over long commitments

The Real Question Isn’t Fixed vs Variable

It’s:

👉 What fits your risk tolerance and plans?

Are you:

- staying long-term?

- planning to move soon?

- comfortable with payment changes?

The Bottom Line

There’s no one-size-fits-all answer in 2026.

The best mortgage isn’t just about the lowest rate — it’s about choosing the structure that fits your life.