One of the most common questions I’m hearing right now is:

“Should I wait until rates drop before buying or refinancing?”

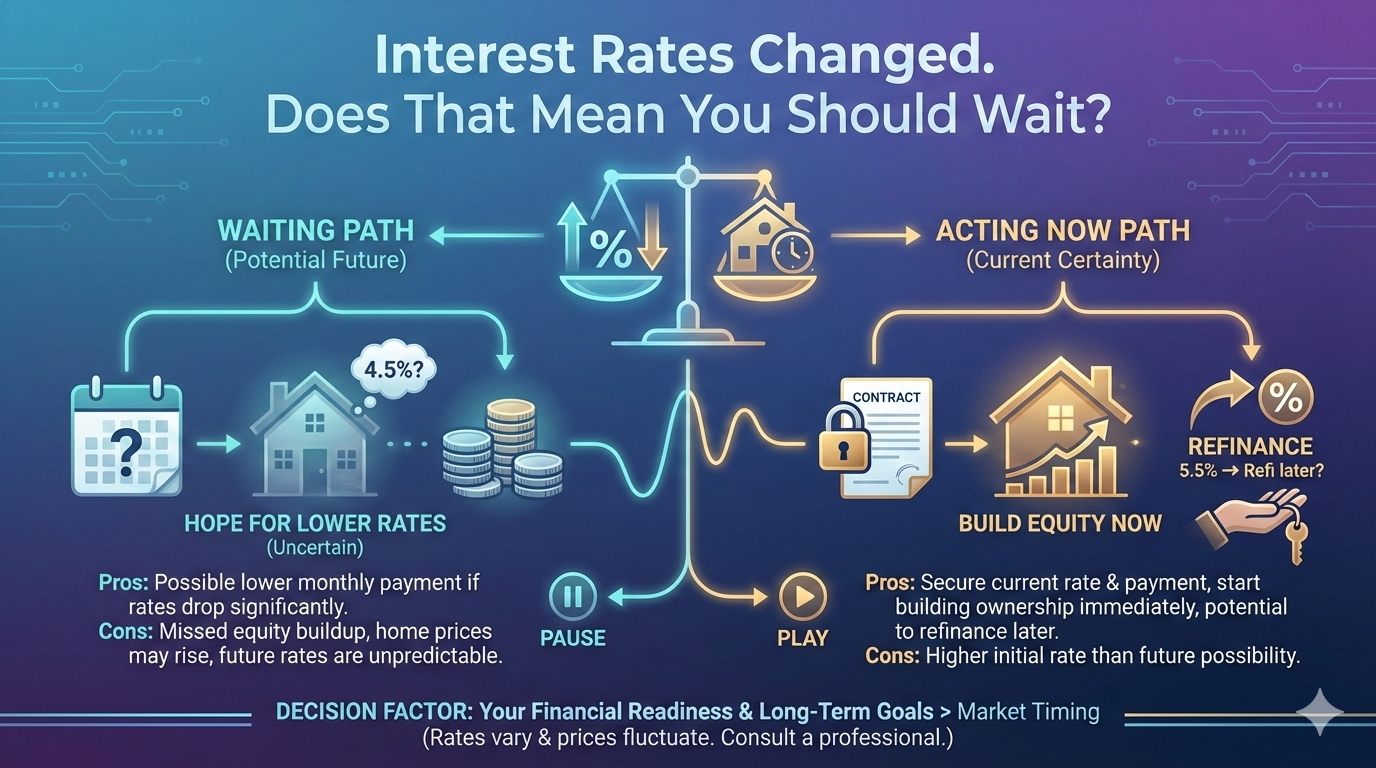

It’s a fair question. Interest rates have moved significantly over the past couple of years in Canada, and naturally, people want to time the market. But when it comes to mortgages, timing the market perfectly is almost impossible — and waiting can sometimes cost more than acting strategically.

Here’s why.

1. Rates Move Faster Than Buyers Do

By the time rate cuts are officially announced by the Bank of Canada, the market has often already adjusted. Lenders price in expectations early.

When rates begin to drop meaningfully, demand usually increases quickly. More buyers enter the market. Competition rises. Prices often follow.

Lower rate + higher price = not always a better deal.

2. Purchase Price Impacts You Forever — Rate Is Temporary

Many buyers focus entirely on interest rate. But your purchase price affects:

-

Your down payment

-

Your total mortgage size

-

Your property taxes

-

Your long-term equity growth

Interest rates, on the other hand, change. You can refinance. You can renew. You can restructure.

If you buy at a better price today and refinance when rates fall, you may come out ahead compared to paying significantly more later just to secure a slightly lower rate.

3. Fixed vs Variable: It’s About Strategy, Not Guessing

There isn’t a universal “right” mortgage product right now.

Some borrowers prefer fixed payments for stability and peace of mind.

Others choose variable rates strategically, anticipating future decreases.

The key is structuring the mortgage around:

-

Your income stability

-

Your cash flow comfort

-

Your risk tolerance

-

Your long-term plans

It’s not about predicting headlines. It’s about building flexibility.

4. Qualification Rules Matter More Than Headlines

In Canada, borrowers must qualify under the federal mortgage stress test rules. That means you’re approved at a higher qualifying rate than your contract rate.

So even if rates drop slightly, it doesn’t always dramatically change your approval power. What matters more is:

-

Debt ratios

-

Credit strength

-

Income consistency

-

Down payment structure

A well-prepared application often makes a bigger difference than waiting for a quarter-point rate change.

5. The Bigger Picture: Lifestyle & Financial Position

Mortgage decisions shouldn’t be based solely on rates.

Ask yourself:

-

Is your rent increasing?

-

Do you need more space?

-

Are you planning to stay in the area long term?

-

Would owning improve your financial stability?

Real estate isn’t just an investment vehicle — it’s housing security.

The Bottom Line

Rates will move. They always do.

But trying to perfectly time the lowest point often leads to missed opportunities. In many cases, the smarter move is securing the right property at the right price with a mortgage structured for flexibility.

If you’re unsure whether now is the right time, a quick review of your numbers can give you clarity. No pressure. Just strategy.

Because the right mortgage plan isn’t about guessing the market — it’s about understanding your options.