I’ve had a few clients call me recently, confused about why banks are raising their mortgage rates even though the Bank of Canada has been lowering interest rates. It does feel backwards, but here’s what’s going on.

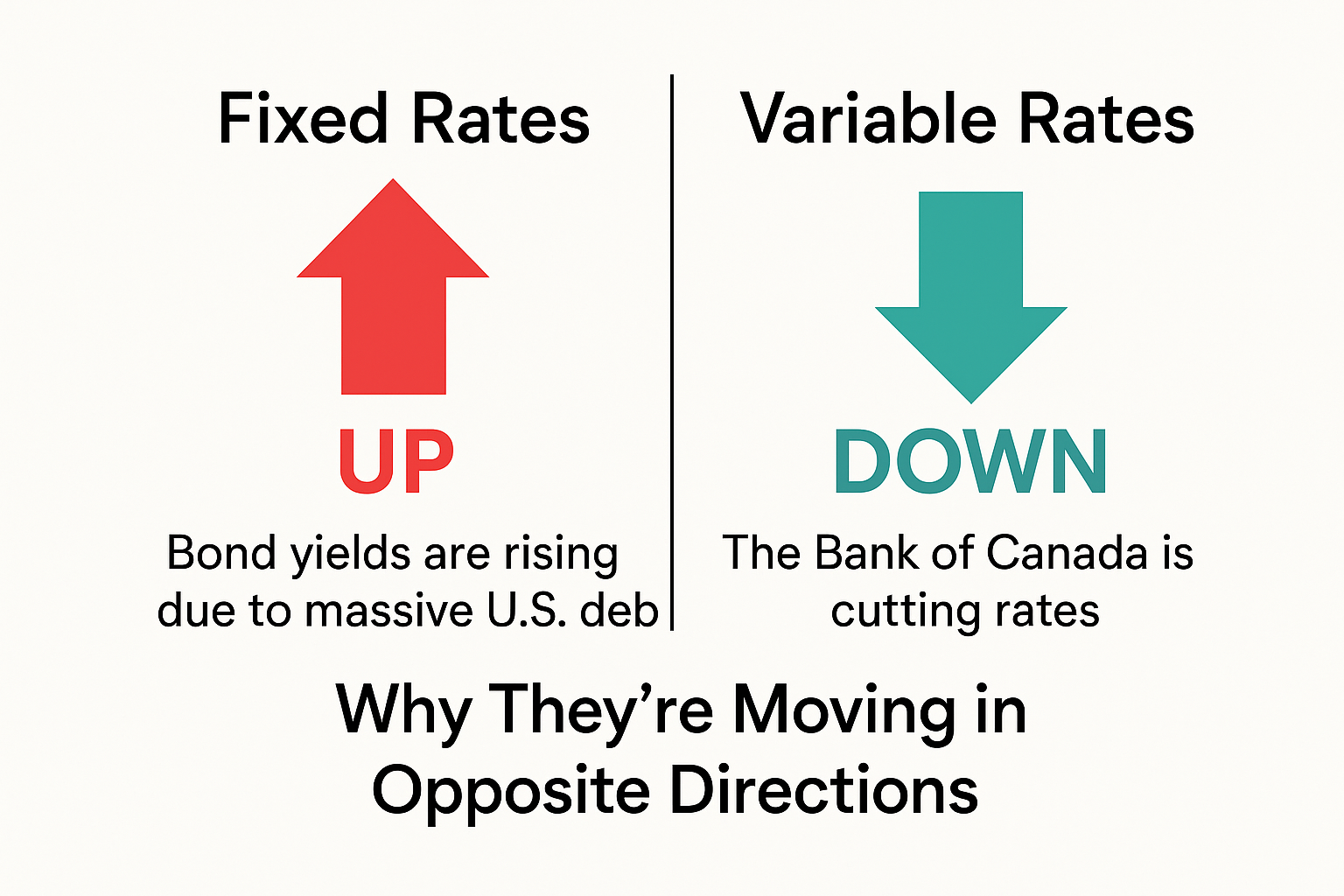

- Fixed mortgage rates are based on bond yields (not directly on the Bank of Canada rate). When bond yields rise, fixed mortgage rates usually go up too.

- Right now, U.S. government debt is climbing by trillions of dollars. To manage that debt, the U.S. sells more bonds. But with so much debt, investors see U.S. bonds as riskier, so they demand higher returns (higher bond yields).

- Higher bond yields = higher fixed mortgage rates here in Canada.

On the other hand:

- Variable mortgage rates do move with the Bank of Canada’s rate. So when the Bank of Canada lowers rates, variable mortgage holders see their payments go down.

- Lower Bank of Canada rates also make it a bit easier to qualify for a mortgage, which is good news for buyers.

So in short:

- Fixed rates are going up because of rising bond yields, especially influenced by U.S. debt levels.

- Variable rates are coming down thanks to the Bank of Canada’s cuts.

That’s why fixed and variable rates are moving in opposite directions right now.

Contact me if you’d like to discuss this. I’m always happy to help break this stuff down!